Advertisement

Advertisement

Dax Index News: Softer Inflation Outlook Lifts Forecast for German Stocks Today

By:

Key Points:

- DAX rises 0.43% to 24,034 as traders eye US-EU trade talks and Eurozone inflation data for market direction.

- US-China trade optimism lifts global risk appetite, supporting German equities amid weaker auto sector.

- DAX outlook hinges on inflation data, ECB stance, and JOLTs Job Openings report later in the session.

DAX Climbs as Focus Shifts to Inflation, the ECB, and Trade Talks

The DAX opened higher on Tuesday, June 3, climbing 0.43% to 24,034 in early trading. Hopes of US-EU trade negotiations resulting in a trade agreement drove demand for DAX-listed stocks. Market Securities CEO Christophe Barraud remarked:

“EU trade chief Sefcovic, US trade rep. Greer to meet Wednesday. EU strongly regrets US decision to raise steel tariffs. EU prepared to impose countermeasures if talks fail.”

Sector Performance

Easing trade tensions drove demand for German-listed auto stocks. Daimler Truck Holding rallied 1%, while BMW advanced 0.33%. Mercedes-Benz Group, Porsche, and Volkswagen also posted early gains.

Tech stocks also advanced in early trading, with Infineon Technologies and SAP climbing 0.83% and 0.84%, respectively.

Eurozone Inflation in Focus

Meanwhile, expectations of multiple ECB rate cuts continued bolstering demand for rate-sensitive stocks after Germany’s HICP dropped from 2.2% in April to 2.1 in May, inching closer to the ECB’s 2% target.

Later in today’s European session, Eurozone inflation figures will fuel speculation about multiple ECB rate cuts. Economists forecast core inflation to fall from 2.7% in April to 2.5% in May. A lower core inflation reading could signal a more dovish ECB stance, driving demand for German stocks. On the other hand, a higher print may temper bets on aggressive ECB policy moves, weighing on the DAX.

Wall Street Advances on US-China Trade Headlines

Wall Street kickstarted the week on a positive footing. Reports of Trump planning to speak with China’s President Xi Jinping boosted demand for risk assets. The US administration also extended the tariff pause on certain Chinese goods until August 31.

On June 2, the Nasdaq Composite Index and S&P 500 gained 0.67% and 0.41%, respectively, while Dow rose 0.08%.

US Labor Market in the Spotlight

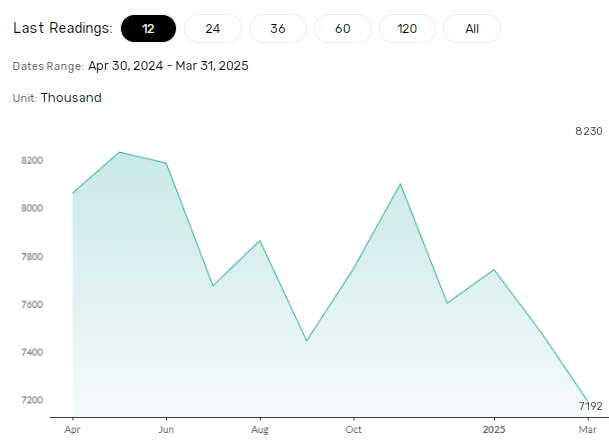

Late in the European session, investors will consider the JOLTs Job Openings data. Economists forecast job openings to fall from 7.192 million in March to 7.1 million in April. A larger-than-expected fall could raise concerns about the US labor market and the economy, impacting risk assets, including the DAX.

A deteriorating labor market may dampen wage growth, pressuring consumer sentiment and spending. Waning consumer spending could fuel recession jitters as private consumption contributes over 60% to the US GDP. Conversely, a higher reading may ease recessionary concerns, bolstering risk sentiment.

Beyond the data, central bank commentary and trade developments will continue influencing market sentiment.

Near-Term Outlook

The DAX’s near-term price trajectory hinges on upcoming economic data, trade headlines, and central bank signals.

- Bearish Scenario: Hotter inflation, US recession fears, rising trade tensions, and hawkish cues could send the index toward 23,500.

- Bullish Scenario: Softer inflation, easing US recession concerns, dovish central bank rhetoric, and easing US-EU trade developments may drive it toward 24,500.

More information in our economic calendar

DAX Technical Indicators

Daily Chart

Despite Monday’s loss, the DAX trades above the 50-day and 200-day Exponential Moving Averages (EMA), preserving its bullish trend.

A sustained move above 24,000 could push the index to the May 28 record high of 24,326. Increasing buying pressure may pave the way to 24,500.

On the downside, a drop below 23,750 could expose the 23,750 level, with 23,500 the next key support level.

The 14-day Relative Strength Index (RSI) at 61.74 indicates the DAX has room to revisit 24,326 before entering overbought conditions (RSI > 70).

Final Thoughts

Volatility will likely continue as investors react to US-EU trade news, central bank rhetoric, and incoming macroeconomic data. German equities also remain exposed to fiscal developments. Traders should stay attuned to both technical and fundamental drivers.

About the Author

Bob MasonChief Crypto Boss

123456789 30 He has written extensively for a broader audience and his current focus is on developments relating to the financial markets including, but not limited to currencies, commodities, alternative asset classes, and global equities.

Advertisement