Advertisement

Advertisement

Nikkei 225 Rises 0.55% as USD/JPY Stabilizes; BoJ Rate Delay Boosts Sentiment

By:

Key Points:

- China’s Ministry of Finance briefing sparks speculation over potential stimulus as Mainland equities suffer heavy losses.

- Nikkei 225 inches up 0.55%, boosted by hopes that the BoJ will delay rate cuts until 2025; USD/JPY steadies after Thursday's dip.

- ASX 200 tracks Wall Street’s decline as mining and banking stocks fall; Fortescue and BHP lead losses with a 1.32% drop in iron ore.

In this article:

US Equities Slip Amid Mixed Inflation and Labor Data Signals

On Thursday, October 10, US Equity Markets ended the session in negative territory as investors digested crucial US economic indicators.

The S&P 500 declined by 0.21%, while the Dow and the Nasdaq Composite Index fell by 0.14% and 0.05%, respectively.

US Inflation and Labor Market Data Muddy the Fed’s Rate Path

On Thursday, the core annual inflation rate rose from 3.2% in August to 3.3% in September. The hotter print could have impacted expectations of multiple Q4 2024 Fed rate cuts.

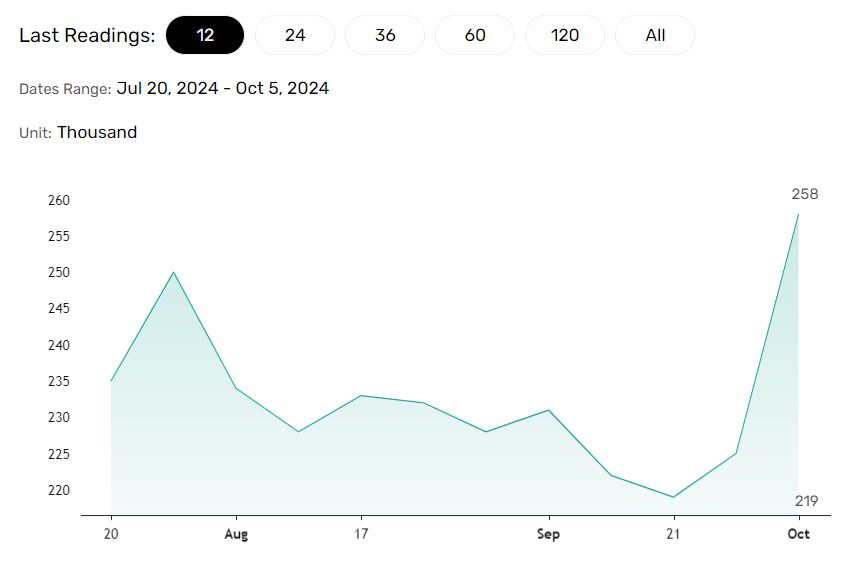

However, the weekly jobless claims data overshadowed the CPI Report. Initial jobless claims jumped from 225k (week ending September 28) to 258k (week ending October 5). Growing concerns about the US labor market could weigh heavily on the Fed’s interest rate decision at the November 6-7 FOMC Meeting. The labor market has recently gained prominence.

Expert Views on the US Labor Market

Arch Capital Global Chief Economist Parker Ross highlighted the need to analyze the weekly jobless claims data at the state level, saying,

“Going forward, we are likely to see further increases in claims as the full impact of Hurricane Helene is processed. We’ll also start to see Hurricane Milton impacts in the weeks ahead, which will leave the labor market outlook muddled. Challenges with the seasonal adjustment factors will also put upward pressure on claims into year-end, most notably for continuing claims.”

China’s Ministry of Finance Briefing Crucial for the Equity Markets

Mainland China equity markets and the Hang Seng Index reacted adversely to Tuesday’s National Development and Reform Commission (NDRC) press conference. The absence of fresh stimulus measures fueled a market rout that left the Hang Seng Index with a loss of 6.53% for the week.

China’s Ministry of Finance (MoF) is expected to hold a press conference on Saturday, October 12, fueling market speculation about a potential stimulus package. While the markets are closed on Saturday, speculation about potential policy measures may impact risk sentiment.

Mainland China Equities Suffer Pre-MoF Press Conference Jitters

In Asia, the Mainland China equity markets suffered heavy losses in the Friday morning session. The CSI 300 was down 1.64%, while the Shanghai Composite declined by 1.18%.

Uncertainty about China’s stimulus plans and the effectiveness of recently rolled out measures impacted investor sentiment.

There was no trading in Hong Kong due to the Ching Ming holiday, and the Hang Seng Index remained closed.

Nikkei Index Inches Higher as USD/JPY Steadies

Meanwhile, the Nikkei 225 advanced by 0.55% on Friday morning, as the USD/JPY pair steadied after Thursday’s drop below 149. Despite Thursday’s pullback, hopes of the Bank of Japan delaying interest rate cuts until Q1 2025 boosted buyer demand for Nikkei 225-listed stocks. The US futures were also modestly higher, supporting the morning gains.

Notable stock movers included Fast Retailing Co. Ltd. (9983), which was up 3.80%, while Sony Corp. gained 0.76%.

ASX 200 Tracks Wall Street into the Red

On Friday, the ASX 200 Index declined by 0.14% during the morning session. Banking and mining stocks contributed to the morning pullback.

Mining giants Fortescue Ltd (FMG) and BHP Ltd. (BHP) saw losses of 1.32% and 0.35%, respectively. Iron ore spot reflected market apprehension ahead of Saturday’s MoF press conference, falling by 1.20% on Friday morning.

Uncertainty about the Fed rate path, following the overnight US data, weakened demand for high-yielding banking stocks. Commonwealth Bank of Australia (CBA) and Westpac Banking Corp. (WBC) saw losses of 0.65% and 0.36%, respectively.

However, overnight gains in gold and oil prices helped limit the ASX 200’s losses, supporting demand for gold and oil-related stocks.

Looking Ahead

Investors should remain alert, focusing on Beijing, the central banks, and the Middle East. Closely monitor news wires, real-time data, and expert commentary to adjust your trading strategies accordingly. Stay updated with the latest news and analysis to effectively manage positions across the Asian equity markets.

About the Author

Bob MasonChief Crypto Boss

TEST 30 He has written extensively for a broader audience and his current focus is on developments relating to the financial markets including, but not limited to currencies, commodities, alternative asset classes, and global equities.

Latest news and analysis

Advertisement