Advertisement

Advertisement

Nikkei 225 and ASX 200 Edge Higher as US Labor Market Concerns Persist

By:

Key Points:

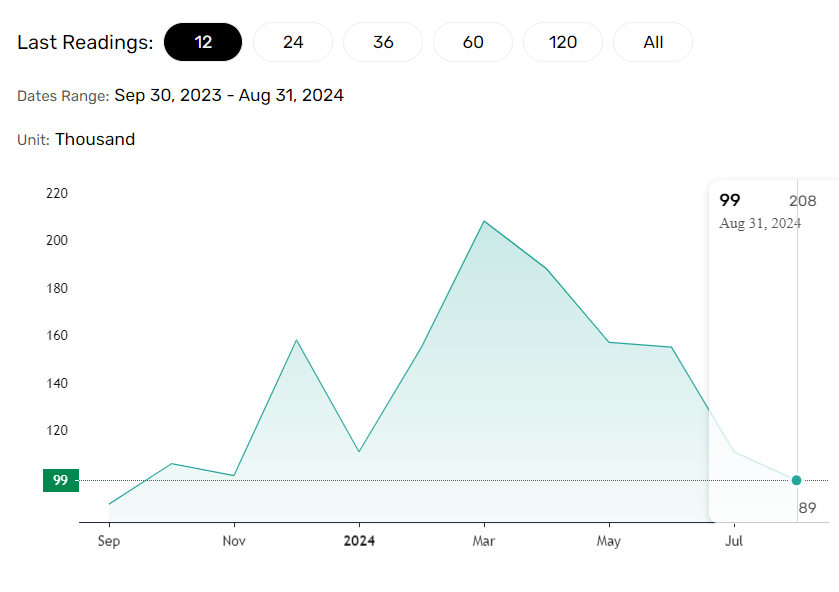

- US labor market data showed weaker job growth in August, with only 99k jobs added vs. 145k expected.

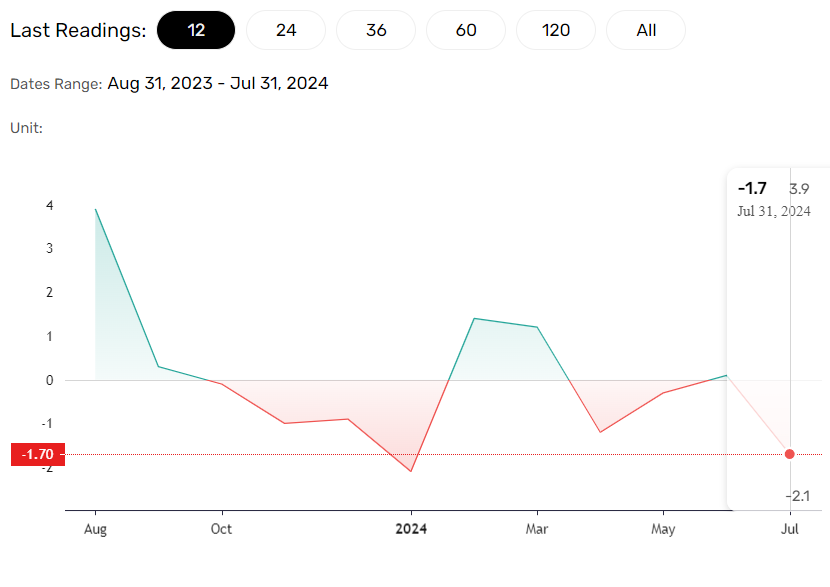

- Japan's household spending fell by 1.7%, easing pressure on the Bank of Japan to raise interest rates.

- Mainland China stocks rose despite tariff concerns as Hang Seng markets remained closed due to weather.

In this article:

US Equity Markets Mixed Ahead of US Jobs Report

On Thursday, September 5, the US equity markets had a mixed session. The Nasdaq Composite Index gained 0.25%, while the Dow and the S&P 500 fell by 0.54% and 0.30%, respectively.

US Labor Market Weakness Dents Risk Sentiment

On Thursday, labor market data triggered investor concerns about the US economy. The ADP reported an employment increase of 99k in August, falling short of a predicted 145k.

A weaker labor market may slow wage growth, possibly curbing consumer spending. Downward trends in consumer spending could impact the US economy as it contributes over 60% to GDP. A US recession may adversely affect the global demand environment, company earnings, and stock prices.

Expert Views on the US Labor Market

Ahead of Thursday’s ADP Report, StoneX Market Analyst David Scutt emphasized the significance of the Report, stating,

“ADP has overstated private US nonfarm payrolls in three of the past four months. Should we see a weak ADP later today, it could point to a really weak NFP (even before BLS overstating concerns are considered).”

Japan: Household Spending Eases BoJ Pressures

In Japan, household spending slid by 1.7% in July after an increase of 0.1% in June.

The fall in household spending may ease pressure on the Bank of Japan to hike interest rates. Downward trends in household spending could dampen demand-driven inflation, supporting a less hawkish BoJ rate path. A less hawkish rate path may affect Yen demand, possibly boosting demand for Nikkei Index-listed export stocks.

The fall in household spending dealt a double blow to the Bank of Japan, which was hoping for increased spending to fuel demand-driven inflation and bolster the economy. Private consumption accounted for 54.3% of GDP in Q2 2024.

Mainland China Markets Rise Despite Tariff Concerns

The Hang Seng Index remained closed on Friday morning due to the HK Observatory hoisting the T8 warning. Subject to weather conditions, the HK markets may resume for afternoon trading.

Meanwhile, the Mainland China markets opened with modest gains. The CSI 300 and the Shanghai Composite rose by 0.30% and 0.34%, respectively, despite concerns about a possible tariff war. Canada and the EU recently targeted China’s electric vehicles (EVs) with tariffs. Notably, the US may also announce plans to increase tariffs on goods from China.

Nikkei Index Edges Higher Amid Weak Household Spending Data

The Nikkei Index rose by 0.04% on Friday morning despite a USD/JPY drop below 143 on Thursday and further downside on Friday. Household spending figures could force the Bank of Japan to delay rate hike discussions, possibly supporting Nikkei Index-listed export stocks. Higher interest rates could boost Yen demand, affecting overseas earnings when converted to Yen.

However, investor caution was evident ahead of the US Jobs Report. Tokyo Electron Ltd. (8035) declined by 1.32%, while Sony Corp. (6758) slid by 2.51%. Nissan Corp. (7201) was down 0.53%.

ASX 200 Gains on the Big Four Banks

The ASX 200 Index advanced by 0.45% on Friday morning. Bank and gold countered losses across the mining and oil stocks. ANZ Group Holdings Ltd. rallied 1.66%, while Northern Star Resources Ltd. (NST) gained 0.96% following a 0.85% rise in gold prices on Thursday.

From elsewhere, iron ore prices continued tumbling on Thursday, impacting the mining giants. BHP Group Ltd (BHP) and Rio Tinto Ltd. (RIO) saw losses of 0.85% and 0.49%, respectively.

Investors should remain alert, with central bank commentary pivotal as the US Jobs Report looms. Closely monitor the news wires, real-time data, and expert commentary to manage trading strategies accordingly. Stay informed with our latest news and analysis to manage positions across the Asian equity markets.

About the Author

Bob MasonChief Crypto Boss

TEST 30 He has written extensively for a broader audience and his current focus is on developments relating to the financial markets including, but not limited to currencies, commodities, alternative asset classes, and global equities.

Latest news and analysis

Advertisement